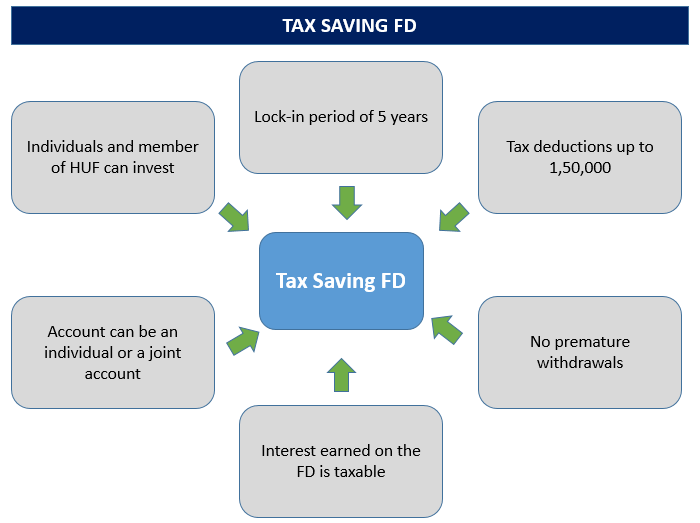

We know that Bank Fixed Deposits /Recurring deposits are the most trusted instruments for savings in our country. The people generally wants to deposit their hard earned money in bank in FDs/RDs. These instruments generated interest income and same is a good source of income for senior citizens. The banks and government have came with various types of instruments in which our senior citizen can invest and earn secure and hassle-free income. The Income Tax Act, 1961 has also provides various rebates and deductions on interest from these FDs/RDs to our citizens.

It important to know various provisions of Income Tax Act, 1961 and other laws so that you can enjoy full benefits of you invested money in these instruments. You also have in your mind those transactions through which your details are shared with the IT Department and for which you are answerable.

PROVISIONS OF INCOME TAX ON INTEREST RECEIVED FROM FDs/RDs

Please note that bank does deduct interest on your saving bank account to the some extent but interest received from FDs/RDs are taxable in head “Income from other sources” if aggregate crossed limit as prescribed under various provisions of Income Tax Act, 1961.

1. SECTION 80TTA- for a resident individual (age of 60 years or less) or HUF, interest earned during a financial year exempt to the extent of Rs. 10,000/- in his Saving Bank Account/Savings Bank Account with Post Office /Co-operative Banks.

Note: – if your income from interest during previous financial year FY 2020-21 is of Rs. 10,100/- then in this case the bank will deduct TDS @10% of whole Rs. 10,100/- and not on Rs. 100/- (Rs. 10,100-Rs.10000).

The exemption will be available on interest earned only from SB Accounts as mentioned above.

This exemption is not available for Senior Citizens (a person being age of 60 years or more).

2. SECTION 80TTB: -Senior citizens (a person being age of 60 years or more), with effect from 1 April 2018, will enjoy an income tax exemption upto Rs 50,000 on the interest income they receive from fixed deposits with banks, post offices etc.

This is applicable on interest received from all types of deposits.

3. Banks are required to deduct tax when interest income from deposits held in all the bank branches put together is more than Rs.40,000 in a year (Prior to FY 2019-20, it was Rs.10,000). A 10% TDS is deducted if PAN details are available. It is 20% if the bank does not have your PAN details.

Note: In case of FDs/RDs you have to check your PAN on the certificates provided to you so that bank officials correctly deduct TDS and file the same in the return. This way you shall claim the same through Form 26AS( Now AIS). If you have not given your PAN then bank will deduct TDS @20% and your TDS amount will not be reflected in your 26AS, this way you will lose chance to claim TDS while filing your return.

LET’S CONSIDER AN EXAMPLE TO CLEAR SOME FACTS TDS ON FDs

Mr. X has invested Rs. 30.00 Lakhs in a five-year FD at @7% p.a. on 01/04/2016;

| Financial Year | Amount of FD | Rate of Interest | Amount of Interest | TDS @10% | Total Balance as on 31st March—— |

| FY 2016-17 | 30,00,000 | 7% | 2,10,000 | 21,000 | 31,89,000 |

| FY2017-18 | 31,89,000 | 7% | 2,23,230 | 22,323 | 33,89,907 |

| FY 2018-19 | 33,89,907 | 7% | 2,37,293 | 23,729 | 36,03,471 |

| FY 2019-20 | 36,03,471 | 7% | 2,52,243 | 25,224 | 38,30,490 |

| FY 2020-21 | 38,30,490 | 7% | 2,68,134 | 26,813 | 40,76,811 |

| Total | 11,90,900 | 1,19,090 |

From above table it is clear that Mr. X will get Rs. 40,76,811 at the time of maturity of his FD and Rs. 1,19,090 has been deduced as TDS from his interest payments. Suppose if Mr. X has not submitted his PAN or his PAN number is wrongly quoted in certificate of FD due to inadvertent of bank official then he will loose claiming of amount of TDS, since it will not show in his 26AS due to wrong PAN and it may be possible that the maturity value he received from bank may be less due to wrong calculation of interest by bank. It is for your benefit to be vigilant and ask from bank interest certificate to check, whether they are calculating interest and TDS as per law or not. It is your right to ask for explanation and statement.

LET’S CONSIDER AN EXAMPLES: Mr. A is a resident Indian having below mentioned incomes;

i) Interest of Rs. 10,000 from SB Account;

ii) Interest of Rs. 1,50,000 from FDs with Canara Bank;

iii) Interest of Rs. 50,000 from FDs with HDFC Bank;

iv) Other income of Rs. 5,00,000.

Let’s calculate Income Tax by considering different situations for Mr. C

| Particulars | Mr. A as normal taxpayer | Mr. A as a Senior Citizen |

| Interest Income | 10,000 | 10,000 |

| Interest from FD Canara Bank | 1,50,000 | 1,50,000 |

| Interest from FD HDFC | 50,000 | 50,000 |

| Other Income | 5,00,000 | 5,00,000 |

| GROSS TOTAL INCOME | 7,10,000 | 7,10,000 |

| Less: deduction u/s. 80TTA | 10,000 | NIL |

| Less: deduction u/s. 80TTB | NIL | 50,000 |

| Taxable Income | 7,00,000 | 6,60,000 |

| Tax ( before rebate 87A) | 32,500 | 28,500 |

| Less: Rebate u/s. 87A | Nil | Nil |

| Tax Payable (including chess @4%) | 33,800 | 29,640 |

Note: Rebate u/s. 87A will be available only in case of taxable income of a resident is Rs. 5.00 Lakhs or below.

Form above it is clear that Senior citizen will pay less tax than an ordinary resident due to rebate given under section 80TTB of the Income Tax Act, 1961.

SOME TIPS TO SAVE TAX, WHILE FILING INCOME TAX RETURN

1. Please note that it is in your favour to file your income tax return and claim TDS as refund in case your net income is within threshold limit or your income during FY is below Rs. 2.50 Lakhs/ Rs. 3.00 Lakhs / Rs. 5.00 Lakhs during previous financial year.

2. A Senior Citizen can claim income from interest to the extent of Rs. 5.00 Lakhs as tax free income. Since threshold limit for Senior Citizen is Rs. 5.00 Lakhs. Please note that if your income from all sources does not exceed Rs. 5.00 Lakhs, then you have to give FORM 15H to the bank declaring that your income from all sources during the current financial year does not exceed Rs. 5.00 Lakhs and the bank on the basis of FORM 15H submitted will not deduct TDS from interest income.

3. You have to submit this FORM 15H in the month of April and FORM 15G is for other Individuals.

4. Please note that the bank will inform details of FDs exceeding Rs. 10.00 Lakhs from all banks in which you have made FDs to the tax authority.

5. The interest received in SB/Post Office/Co-operative Bank will be aggregated from all such accounts you have during a financial year and in same way interest from all FDs will be aggregated for rebate under Section 80TTB.

6. Please note that you have to show in your income tax returns all interest received correctly in the head “Income from other sources”.

7. FDs can be made by depositing of cash also, but you should keep track of cash receipt and source from where you have received cash payment and depositing the same with bank.