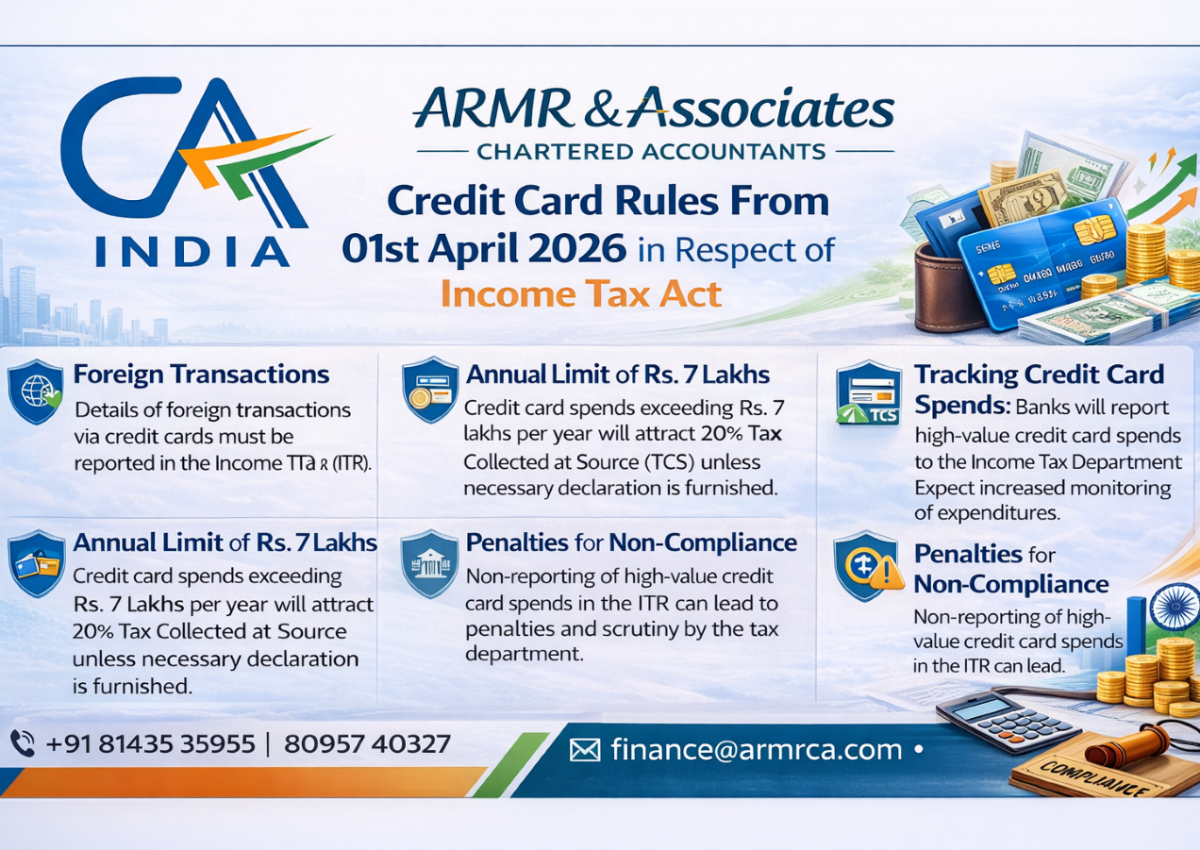

From 1 April 2026, the Income Tax Act, 2025 and the corresponding Income Tax Rules, 2026 will apply to all taxpayers in India. A key focus area of the new regime is the closer monitoring and reporting of high-value credit card transactions. This article explains the key changes that credit card users should be aware of and their practical tax implications.

1. Legal Framework and Effective Date

The Finance Act operationalising the Income Tax Act, 2025 provides that the new law will come into force from 1 April 2026, corresponding to Financial Year (FY) 2026‑27 (Assessment Year 2027‑28). The accompanying Income Tax Rules, 2026 set out the procedural aspects, including reporting obligations for banks and card issuers.

Although there is no separate “credit card tax”, credit card transactions are now squarely integrated into the income tax information system by way of mandatory reporting, Permanent Account Number (PAN) linkage and, in due course, alignment with foreign exchange regulations for overseas spending.

2. Mandatory PAN Linkage for Credit Cards

2.1 Compulsory PAN for Issuance and Continuation

Going forward, credit cards will effectively function as an extension of the holder’s tax identity. Issuers will be required to obtain and verify the PAN of the primary cardholder before issuing or continuing a credit card. In practice, this means:

- New cards will not be issued without a valid PAN (subject to limited exceptions, if any, for small-value or pre‑paid products).

- Existing cardholders whose PAN is not properly linked or verified may face restrictions in credit limits or usage until compliance is completed.

2.2 Impact on KYC and Data Consistency

Banks and financial institutions will be expected to ensure that the PAN, Aadhaar and other KYC details of credit card customers are consistent across savings accounts, current accounts, loans and card portfolios. This will enable the tax department to consolidate information about each taxpayer more accurately, reducing the scope for fragmented or unreported financial activity.

3. Reporting of High-Value Credit Card Transactions

3.1 Statement of Financial Transactions (SFT)

Under the new rules, specified entities such as banks and card issuers will be required to furnish a Statement of Financial Transactions (SFT) for certain high-value credit card activities. While the final notification will define exact thresholds and formats, the broad contours are as follows:

- Annual aggregate card spending beyond a prescribed limit (for example, ₹10 lakh or more per person per issuer in a financial year) will be reportable.

- Large cash repayments of credit card dues (for example, cash payments of ₹1 lakh or more) will be separately flagged.

- High-value international transactions and cross‑border spends may have dedicated reporting fields.

These SFTs will feed into the taxpayer’s Annual Information Statement (AIS) and may be visible in the Form 26AS-equivalent under the new Act.

3.2 Objective of High-Value Reporting

The intention of this reporting is not to levy tax on credit card spending per se, but to identify cases where the lifestyle and spending patterns of an individual appear inconsistent with the income disclosed in the return of income. This will help the department select cases for scrutiny where:

- There is no return of income despite high credit card expenditure.

- Declared income is disproportionately low compared to high-value card spends.

- There are repeated cash repayments of significant amounts without a clear source.

4. Cash Payments Towards Credit Card Dues

4.1 Monitoring Cash Repayments

One of the explicit focus areas is cash deposits or payments used to settle credit card bills. Payments of a substantial amount in cash towards card dues will be reportable. From a risk perspective, taxpayers who frequently clear large card bills in cash can expect closer scrutiny.

4.2 Best Practices for Taxpayers

To mitigate unnecessary questioning, individuals and small business owners should:

- Prefer banking channels (NEFT/RTGS/UPI/cheque) rather than cash for sizeable repayments.

- Maintain clear documentation of the source of funds used for repayments, especially where amounts are large or linked to sale of assets, loans, or business receipts.

- Avoid routing unexplained cash through credit card accounts as a means to mask its origin.

5. Overseas Credit Card Spending and LRS/TCS Linkage

5.1 Alignment with Liberalised Remittance Scheme (LRS)

Historically, foreign spending on international credit cards outside India was not always treated at par with remittances under the Liberalised Remittance Scheme (LRS). Policy announcements have indicated a move towards full alignment so that overseas credit card spends are also counted against an individual’s LRS limit.

Once fully implemented through formal notifications and system changes, the following can be expected:

- Overseas credit card transactions will be aggregated with other LRS remittances for the purpose of monitoring annual limits.

- Data relating to such transactions may be shared with the tax department to monitor compliance.

5.2 Tax Collected at Source (TCS) on Foreign Spends

Under existing LRS rules (as modified from 1 April 2025), TCS applies at specified rates beyond certain thresholds on outward remittances, with concessions for education and medical remittances. As and when international credit card spends are formally brought under LRS and TCS:

- Card issuers or authorised dealers may collect TCS on qualifying overseas transactions in excess of the prescribed threshold.

- Such TCS will be visible in the taxpayer’s AIS and can be claimed as a credit against the final tax liability while filing the return.

Taxpayers who frequently travel abroad or spend in foreign currency using credit cards should monitor the aggregate of their foreign spends across all cards and banks to avoid unexpected TCS outflows.

6. Paying Income Tax Using Credit Cards

6.1 Credit Card as an Accepted Mode of Tax Payment

The new framework also contemplates permitting payment of income‑tax dues through credit cards, in addition to existing modes such as net banking, debit cards, UPI, and over-the-counter challans (where allowed). This can make it easier for taxpayers to discharge tax liabilities within due dates, especially close to deadlines when funds may be temporarily parked in other accounts.

6.2 Points of Caution

While this facility adds convenience, taxpayers should be cautious:

- Credit card interest rates are typically high if dues are not paid in full by the statement due date. Rolling over tax payments can therefore be very expensive.

- Any convenience fees or charges levied by the card issuer or payment gateway should be factored in while assessing the cost of using a card for tax payments.

- For businesses, the accounting treatment of such payments (including the treatment of charges and interest) should be properly documented.

7. Practical Considerations for Different Categories of Users

7.1 Salaried Individuals and HNIs

Salaried individuals and high-net-worth individuals (HNIs) who use multiple premium cards often incur significant annual spends on travel, lifestyle and luxury purchases. Under the new regime:

- High-value spends are more likely to be visible to the department through SFT and AIS.

- It becomes important to ensure that declared income adequately supports the level of expenditure.

- Investments, loans and other sources of funds should be well-documented so that any future inquiries can be answered with ease.

7.2 Proprietors and Small Business Owners

Many proprietors and partners routinely use personal credit cards for business expenses. Under the enhanced reporting environment:

- Clear segregation of business and personal spends is essential, with proper accounting entries and supporting invoices.

- Where business spends are routed through personal cards and reimbursed from business accounts, these movements should be transparently recorded.

- Cash withdrawals or cash repayments linked to business usage should be minimised and, where unavoidable, fully explained in the books.

7.3 Students and Frequent Travellers

Students studying abroad and frequent travellers who use credit cards extensively in foreign currency should:

- Track cumulative foreign spends across cards to ensure compliance with LRS limits.

- Understand when and how TCS may apply on these transactions.

- Maintain supporting documents (admission letters, fee receipts, travel invoices) to demonstrate the purpose of foreign expenditure, particularly where concessional TCS rates or exemptions are claimed.

8. Documentation, AIS Reconciliation and Scrutiny Risk

8.1 Annual Information Statement (AIS) and Form 26AS

With the expansion of credit card reporting, more taxpayers will see card‑related entries in their AIS or equivalent information statements. It is advisable to:

- Review AIS annually and reconcile high‑value spends with known card usage.

- Identify any mismatches or errors early and take up rectification with the bank or issuer, if needed.

- Ensure that the pattern of spending is consistent with the income profile reported in the return.

8.2 Handling Notices and Queries

If selected for scrutiny or if an automated communication is issued based on AIS mismatch or high‑spend flags, taxpayers should be prepared to:

- Provide card statements for the relevant period.

- Explain sources of funds for repayments, particularly for large cash payments or balance transfers.

- Demonstrate the business or personal nature of specific transactions, where relevant.

A proactive approach to documentation and reconciliation can significantly reduce the stress and effort involved in responding to such notices.

9. Key Takeaways and Action Points

For individual taxpayers and small businesses, the key action points in light of the new credit card rules from 1 April 2026 are:

- Ensure PAN is correctly linked and updated with all card issuers.

- Avoid large cash repayments; use traceable banking channels wherever possible.

- Maintain clear documentation for both domestic and overseas card spends.

- Monitor AIS and other information statements annually and reconcile card‑related entries.

- For overseas transactions, track cumulative LRS‑linked spends and factor in potential TCS.

- Seek professional advice where there is a significant gap between lifestyle spending and reported income.

These measures will not only support income tax compliance but also reduce the likelihood of disputes, penalties or prolonged assessments in the evolving data‑driven tax environment.