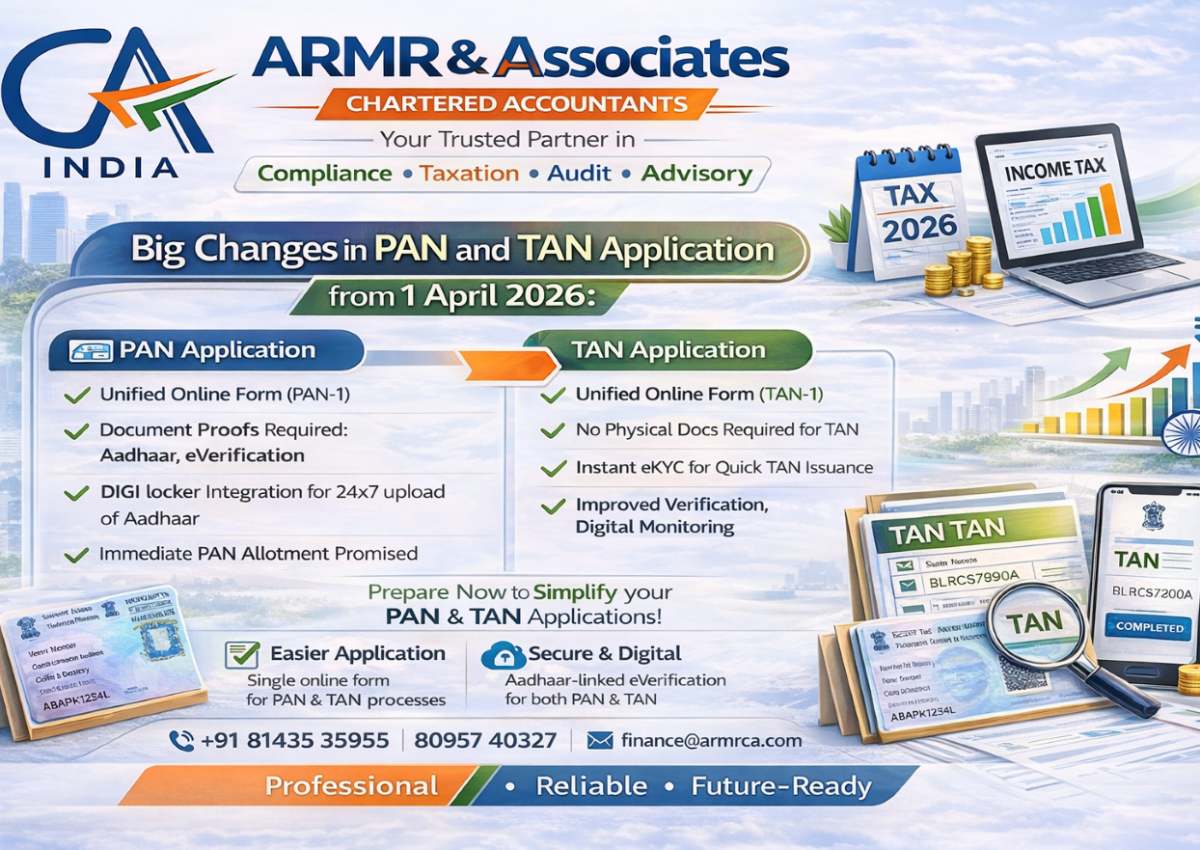

From 1 April 2026, the process of applying for PAN and TAN is undergoing a significant overhaul under the new Income‑tax framework. These changes impact both first‑time applicants and those seeking corrections or updates, and will directly affect individuals, businesses, and tax professionals.

Why these changes now?

The government’s stated objectives are to strengthen identity verification, reduce misuse of PAN/TAN, and align the data architecture with the upcoming regime under the new Income‑tax Act, 2025. PAN is being positioned as the central financial identifier, and TAN as a cleaner compliance key for TDS/TCS deductors.

PAN: What changes from 1 April 2026?

1. Aadhaar‑only PAN applications discontinued

Till 31 March 2026, an individual can apply for PAN using only Aadhaar as proof (including as proof of date of birth). From 1 April 2026, Aadhaar alone will no longer be sufficient; additional documents will be mandatory.

Key points:

- Aadhaar‑only PAN applications are allowed only up to 31 March 2026.

- From 1 April 2026, separate proof of date of birth and other KYC documents must be furnished even if Aadhaar is seeded.

2. Additional documents now compulsory

From 1 April 2026, applicants must furnish specific documents in addition to Aadhaar for identity, address, and date of birth.

Illustrative list (exact combination may vary by category):

- Birth certificate

- Voter ID

- Class 10 certificate

- Passport

- Driving licence

- Magistrate affidavit or other notified documents

For taxpayers, this means document readiness and consistency across KYC records will become critical at the application stage itself.

3. PAN name must match Aadhaar

The name printed on PAN must now strictly match the name as per Aadhaar. Any mismatch can lead to application rejection or future issues while linking and during high‑value transactions.

Practical steps:

- Correct Aadhaar details first (spelling, initials, order of names).

- Use the exact same format when filing the new PAN form or requesting a change.

New PAN forms replacing old 49A / 49AA

One of the most visible changes is the replacement of existing PAN application forms with new, category‑specific forms. Old forms (like Form 49A and 49AA) will not be accepted for fresh applications or corrections from 1 April 2026.

Indicative new PAN forms:

- Form 93 – PAN application for Indian individuals (replacing 49A for individuals).

- Form 94 – PAN application for Indian companies and other Indian entities.

- Form 95 – PAN application for non‑resident / foreign individuals (replacing 49AA for individuals).

- Form 96 – PAN application for foreign companies / foreign entities.

These forms will be used on or after 1 April 2026 on the authorised platforms (Protean, UTIITSL, and the Income‑tax e‑filing portal). Old versions will become invalid for processing.

The application channels, however, remain familiar:

- Protean (formerly NSDL e‑Gov)

- UTIITSL

- Income‑tax Department’s e‑filing portal

PAN usage: Higher thresholds and broader coverage

Along with application rules, the thresholds and scope for mandatory quoting of PAN in high‑value transactions are being re‑aligned with the new law.

Indicative changes:

- Deposits/withdrawals: PAN required if aggregate cash deposits or withdrawals in a financial year reach ₹10 lakh or more.

- Motor vehicles (including two‑wheelers): PAN required for purchase where value exceeds ₹5 lakh.

- Hotel/restaurant/events: PAN mandatory where a single payment exceeds ₹1 lakh.

- Immovable property: PAN required when transaction value exceeds ₹20 lakh.

These revised limits need to be factored into documentation and TDS/TCS checks, especially for real estate, hospitality, and automobile transactions.

TAN: Changes from 1 April 2026

While PAN changes have been more widely discussed, TAN‑related changes are also being aligned with the new rules and forms effective 1 April 2026. New or revised TAN application and correction forms are expected to come into effect alongside the new PAN forms.

Likely areas of change:

- New TAN application form codes replacing the existing generic TAN application/correction forms.

- Updated fields to capture detailed deductor information in line with the new Act.

- Stricter validation for category of deductor (company, firm, government office, local authority, etc.), registered address, and responsible person details.

Deductors should assume that old TAN forms may not be accepted for fresh allotments or corrections made after 1 April 2026 and should monitor updates from the Income‑tax Department and facilitation centres.

Impact for taxpayers, businesses and professionals

For individuals

- Last chance to use the Aadhaar‑only PAN route is 31 March 2026.

- Ensure Aadhaar, birth certificate, and school/identity documents are aligned to avoid rejections.

- Be prepared to quote PAN in more financial and property‑related transactions than before.

For businesses and deductors

- Update internal KYC checklists with the new PAN and TAN form numbers and document requirements.

- Train staff handling onboarding, payroll, vendor payments, and TDS/TCS to capture PAN/TAN correctly under the new forms.

- Review transaction flows (cash, property, vehicle, hotel/event spends) to ensure PAN is collected wherever new thresholds are triggered.

For professionals (CAs, consultants, brokers)

- Update engagement letters and checklists for PAN/TAN application support.

- Inform clients about the 31 March 2026 cut‑off for Aadhaar‑only PAN and the need to keep additional documents ready.

- Factor new PAN quoting requirements into transaction structuring, documentation, and compliance reviews.

Action points: Before and after 1 April 2026

Before 31 March 2026

- If you or your clients do not have PAN, consider applying under the current Aadhaar‑only route while it is still available.

- Rectify name/date‑of‑birth mismatches in Aadhaar to avoid future rejections.

- Complete pending corrections in PAN/TAN where old forms and relaxed KYC still apply.

From 1 April 2026 onwards

- Use only the new PAN forms (Forms 93–96) as applicable; do not use old 49A/49AA formats.

- Keep additional documents ready for identity, address, and date‑of‑birth proof in all PAN applications.

- Monitor official announcements for the notified new TAN forms and ensure all new TAN allotment/correction applications use the updated formats.

- Review internal documentation processes for high‑value transactions to align with revised PAN quoting thresholds.

Final thoughts

The 1 April 2026 changes mark a shift from a relatively relaxed PAN/TAN framework to a more structured, documentation‑heavy, and analytics‑driven system. For taxpayers and businesses, the key will be preparedness: keeping documents in order, switching to the new forms, and embedding these requirements into everyday transaction workflows.