Applicable for FY 2025–26 and FY 2026–27

Residential status is determined separately for each financial year and directly governs the scope of income taxable in India. The underlying day-based conditions remain aligned for FY 2025–26 and FY 2026–27; from FY 2026–27 onwards, they operate under the re‑enacted framework of the Income-tax Act, 2025.cleartax+1

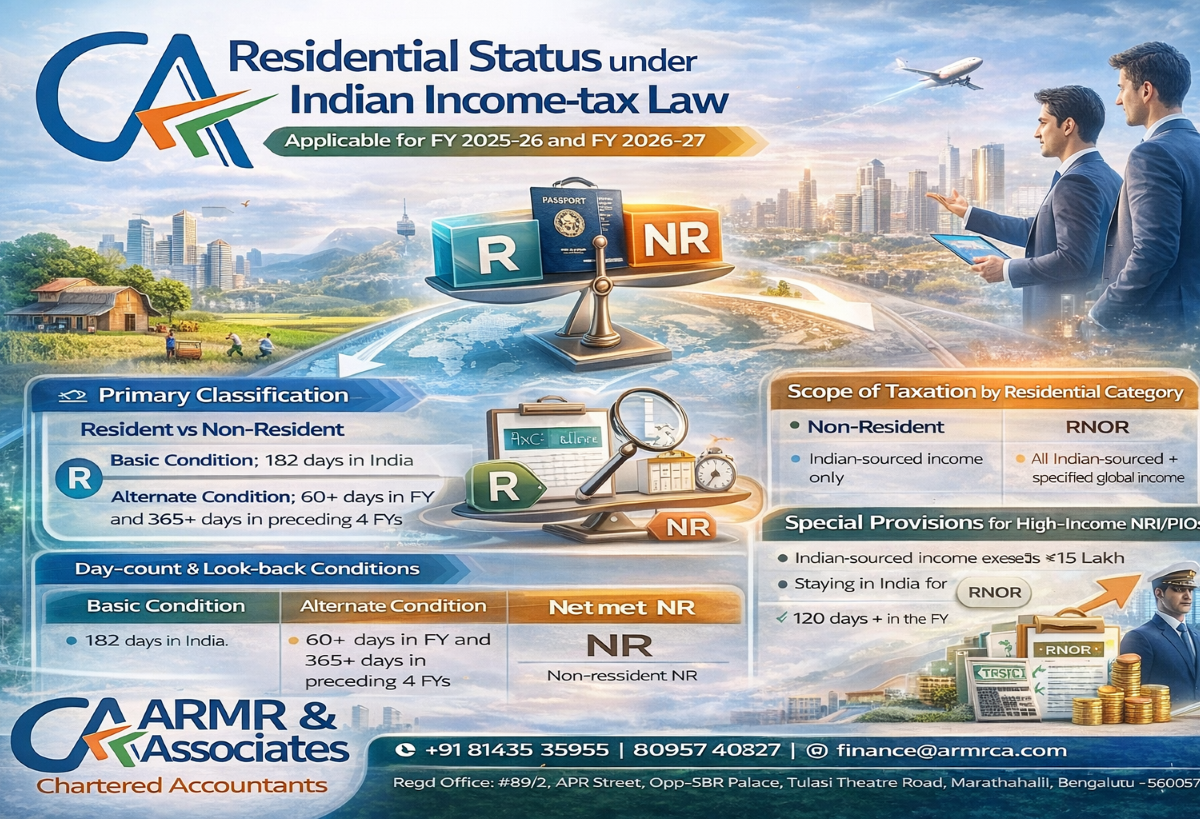

1. Primary classification – Resident vs Non-Resident (individuals)

For each financial year, an individual is first classified as Resident or Non-Resident (NR) based on the number of days of physical presence in India.taxguru+2

1.1 Day-count conditions

| Condition label | Objective criteria in the relevant FY | Residential outcome |

| Basic residency condition | Presence in India for 182 days or more | Treated as Resident |

| Alternate residency condition | Presence in India for 60 days or more in that FY and 365 days or more during the 4 immediately preceding FYs (subject to specific relaxations for certain categories of Indian citizens/PIOs) | Treated as Resident |

| Where neither condition is fulfilled | – | Treated as Non-Resident (NR) |

Special relaxations can extend the 60‑day threshold (for example, for certain Indian citizens leaving India for employment, or visiting India), but the above framework remains the starting point.

2. Secondary classification – ROR vs RNOR (for Residents)

Once an individual is determined to be Resident for a particular year, they are further classified as either:motilaloswal+2

- Resident and Ordinarily Resident (ROR), or

- Resident but Not Ordinarily Resident (RNOR)

2.1 Look-back criteria

| Residential category | Historical presence and residency criteria | When applicable |

| Resident and Ordinarily Resident (ROR) | (a) Resident in India in at least 2 out of 10 preceding financial years, and (b) Physically present in India for 730 days or more during the 7 preceding financial years | Both conditions satisfied |

| Resident but Not Ordinarily Resident (RNOR) | Individual is Resident in the relevant FY but does not satisfy one or both of the above conditions | At least one condition not satisfied |

2.2 Scope of taxation by residential category

| Category | Scope of income taxable in India |

| Non-Resident (NR) | Income received or deemed to be received in India; income accruing or deemed to accrue or arise in India |

| RNOR | All Indian-sourced income, plus only specified foreign-sourced income (typically, income from a business controlled in or a profession set up in India) |

| ROR | Global income (Indian and foreign sourced) |

3. Special provisions for certain Indian citizens / PIOs (high-income)

Additional residency provisions apply to certain high-income Indian citizens and Persons of Indian Origin (PIOs) with significant Indian-sourced income, particularly NRIs frequently visiting India.

3.1 Enhanced 120‑day presence criterion

| Parameter | Requirement | Consequence |

| Indian-sourced income (excluding foreign-sourced income) | Exceeds ₹15 lakh in the relevant FY | Triggers enhanced review |

| Physical presence in India | 120 days or more but less than 182 days in that FY and 365 days or more during the preceding 4 financial years | Individual is treated as Resident for that FY, generally falling under RNOR if look-back criteria are not fully met |

3.2 Deemed resident provision

| Parameter | Requirement | Consequence |

| Citizenship | Indian citizen | – |

| Indian-sourced income (excluding foreign-sourced income) | Exceeds ₹15 lakh in the relevant FY | – |

| Tax position outside India | Individual is not liable to tax in any other country | Treated as a deemed Resident of India (typically RNOR) |

motilaloswal+1

4. Comparative view – FY 2025–26 vs FY 2026–27

From an advisory and compliance perspective, the computational approach remains substantially consistent across both years; only the legislative framework transitions to the Income-tax Act, 2025 from FY 2026–27.counselvise+2

| Aspect | FY 2025–26 (AY 2026–27) | FY 2026–27 (AY 2027–28) |

| Governing statute | Income-tax Act, 1961 | Income-tax Act, 2025 |

| Core day-based criteria | 182‑day condition; 60‑day + 365‑day condition with specified relaxations | Substantively similar conditions carried forward |

| High-income NRI rules | Enhanced 120‑day presence with ₹15 lakh threshold; deemed resident concept | Same policy design reflected in the new Act |

| Final residential buckets | NR, RNOR, ROR | NR, RNOR, ROR |

In practice, existing day-count working papers, RNOR assessments and NRI residency review frameworks remain usable, with updates only to section references and citations under the new Act.

5. Seafarers and merchant navy personnel – specific rule from FY 2026–27

For Indian citizen seafarers (merchant navy and similar crew), the Income-tax Rules, 2026 introduce a formalised mechanism for excluding certain voyage days when computing stay in India for residential status from FY 2026–27 onwards.

| Item | Treatment under Rule 8 (from FY 2026–27) |

| Category of individual | Indian citizen, member of the crew of a foreign-bound ship |

| Exclusion from “stay in India” | Period commencing from the date of joining the ship to the date of signing off from the ship, as recorded in the Continuous Discharge Certificate (CDC), in respect of an eligible voyage |

| “Eligible voyage” | Voyage of a ship engaged in carriage of passengers or freight in international traffic where: (a) it originates from a port in India and has its destination at a port outside India, or (b) it originates from a port outside India and has its destination at a port in India |

| Practical impact | The excluded voyage period is not counted as days of stay in India, which can shift the individual’s status from Resident to RNOR or NR, depending on overall day-count and past presence |