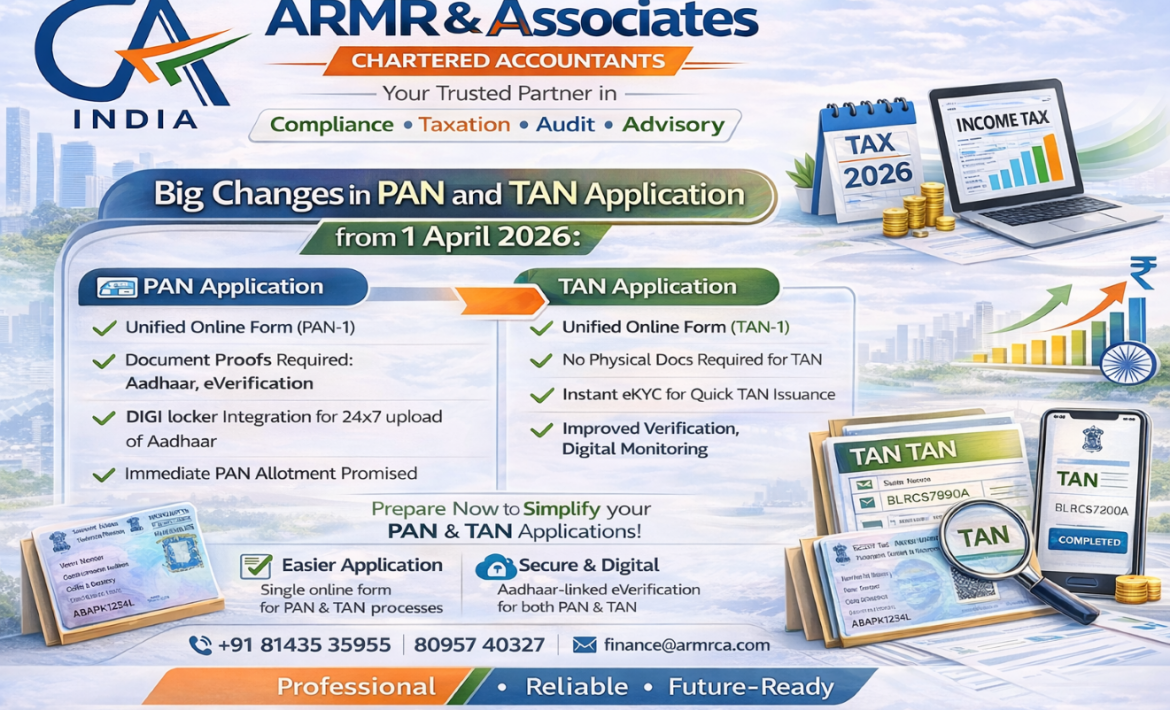

Big Changes in PAN and TAN Application from 1 April 2026: What Taxpayers Must Know

From 1 April 2026, the process of applying for PAN and TAN is undergoing a…

From 1 April 2026, the process of applying for PAN and TAN is undergoing a…

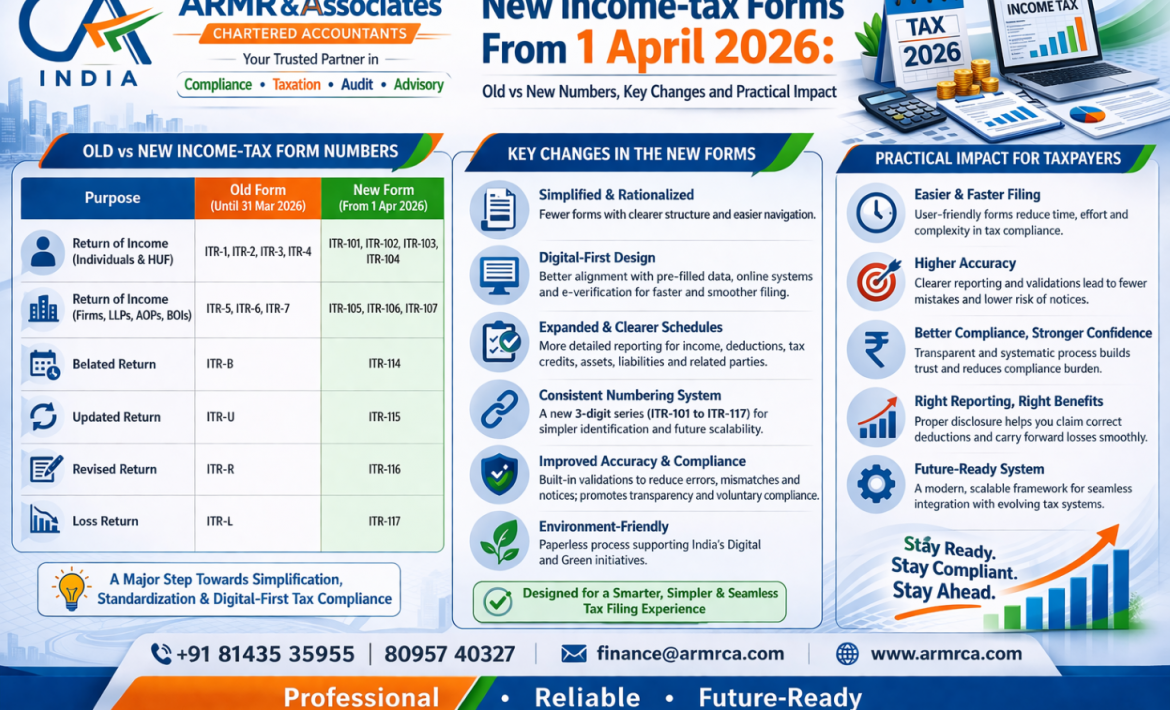

From 1 April 2026, the Income‑tax compliance landscape is changing significantly. The new Income‑tax Act,…

From 1 April 2026, the old Income‑tax Act, 1961 is replaced by the new Income‑tax…

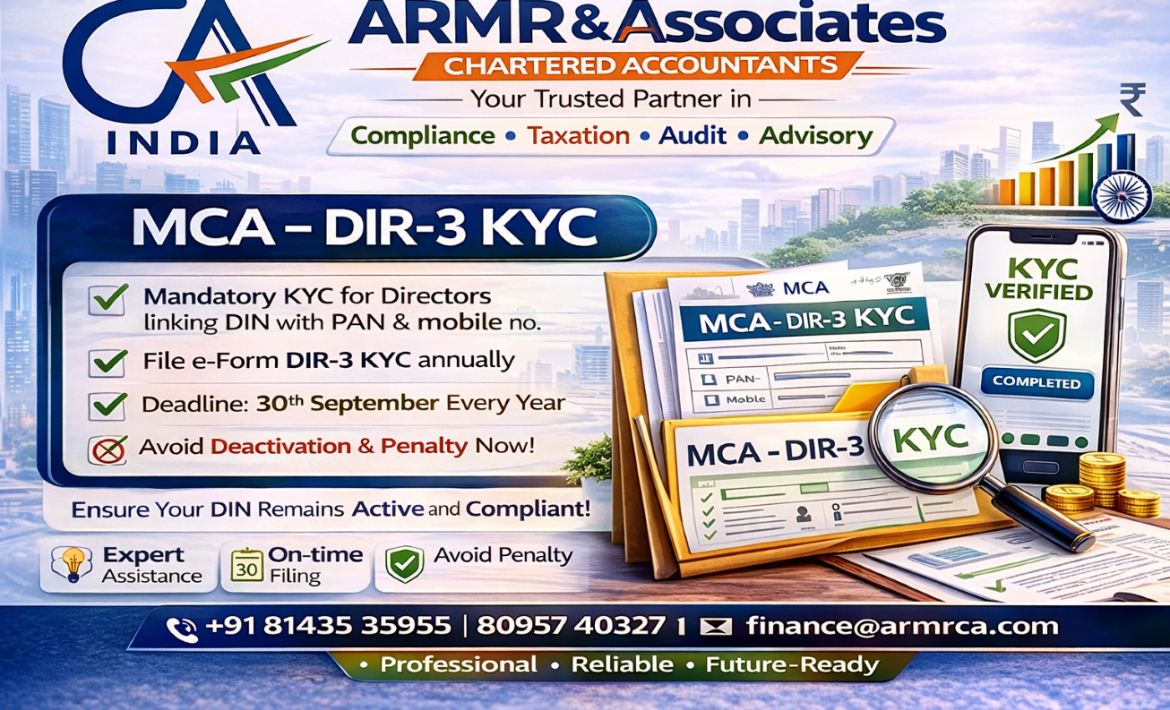

1. Background – What is DIR‑3 KYC? Every individual who holds a Director Identification Number…

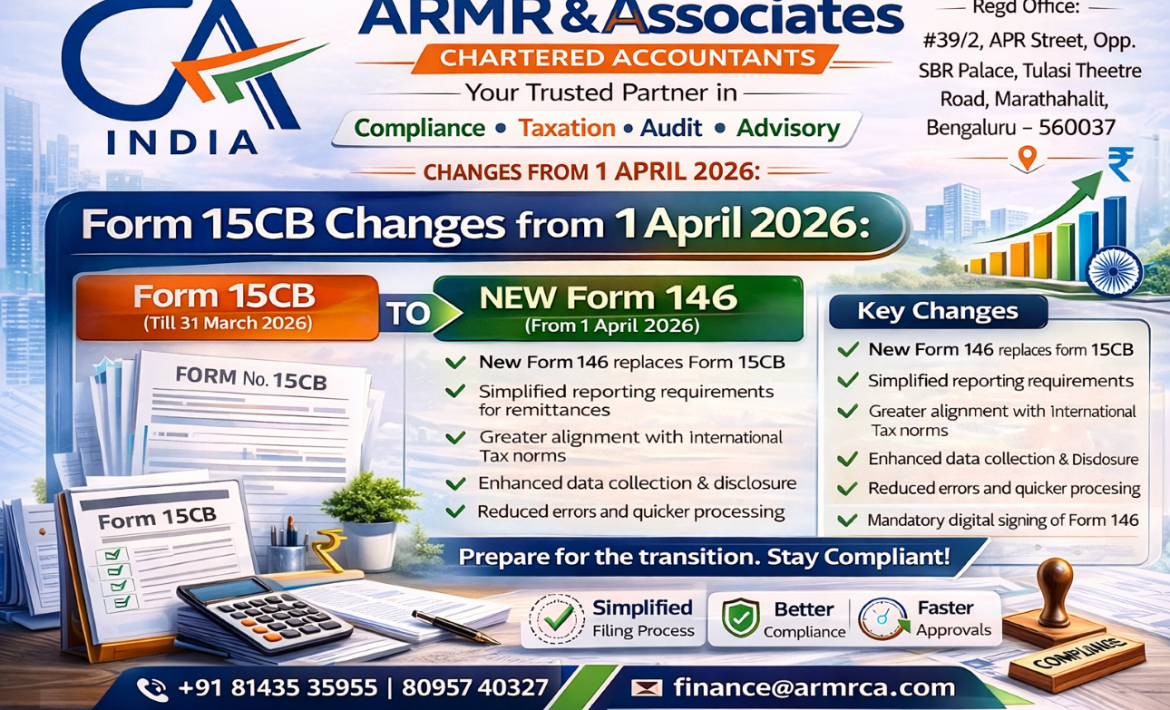

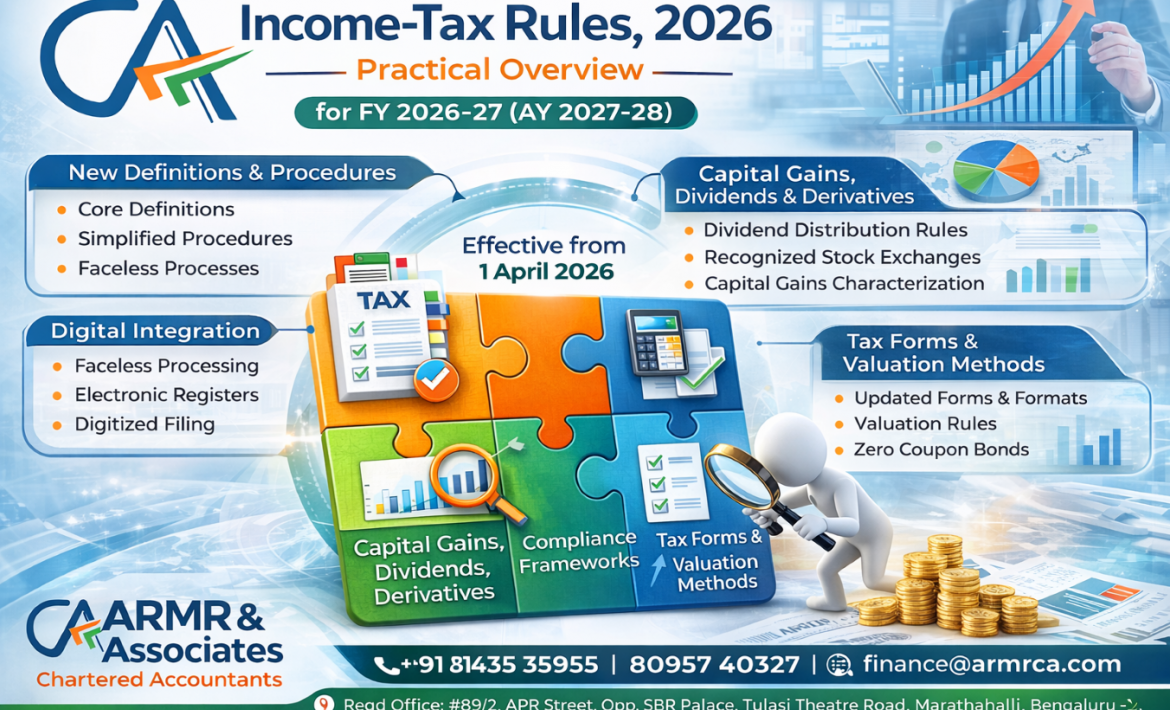

From 1 April 2026, the Income Tax Act, 2025 and the corresponding Income Tax Rules,…

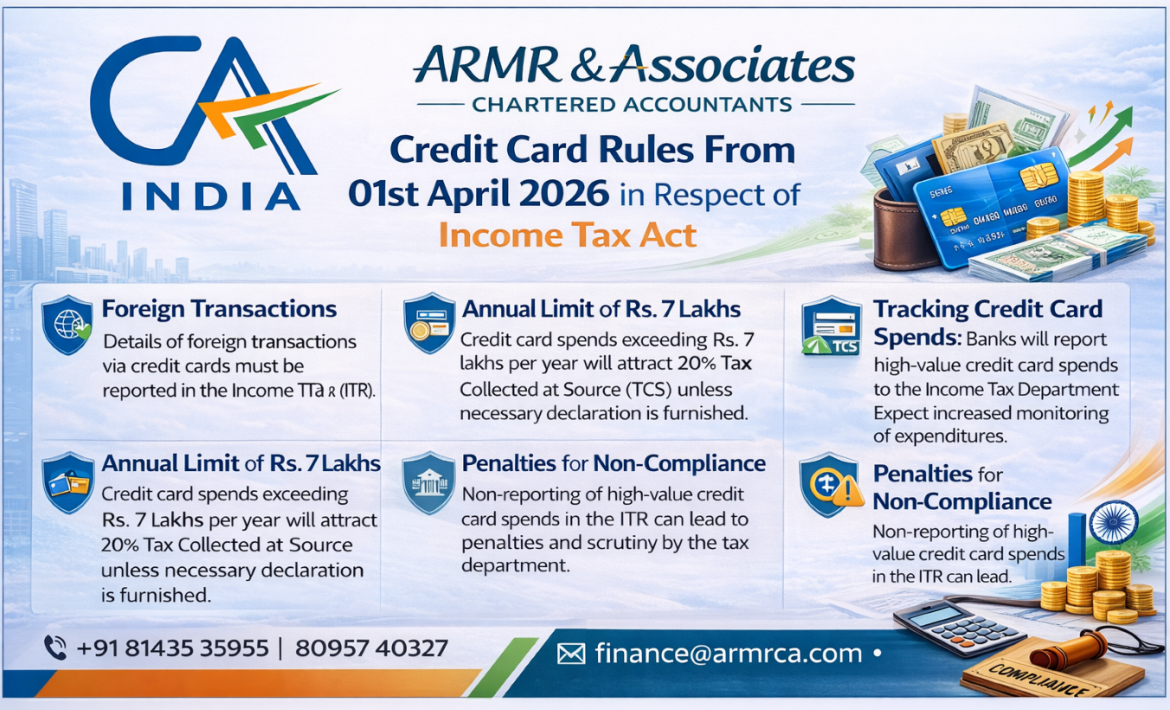

India has seen a sharp rise in equity, intraday and derivatives trading in recent years.…

Running a business today requires more than just sales and operations—it also means staying updated…

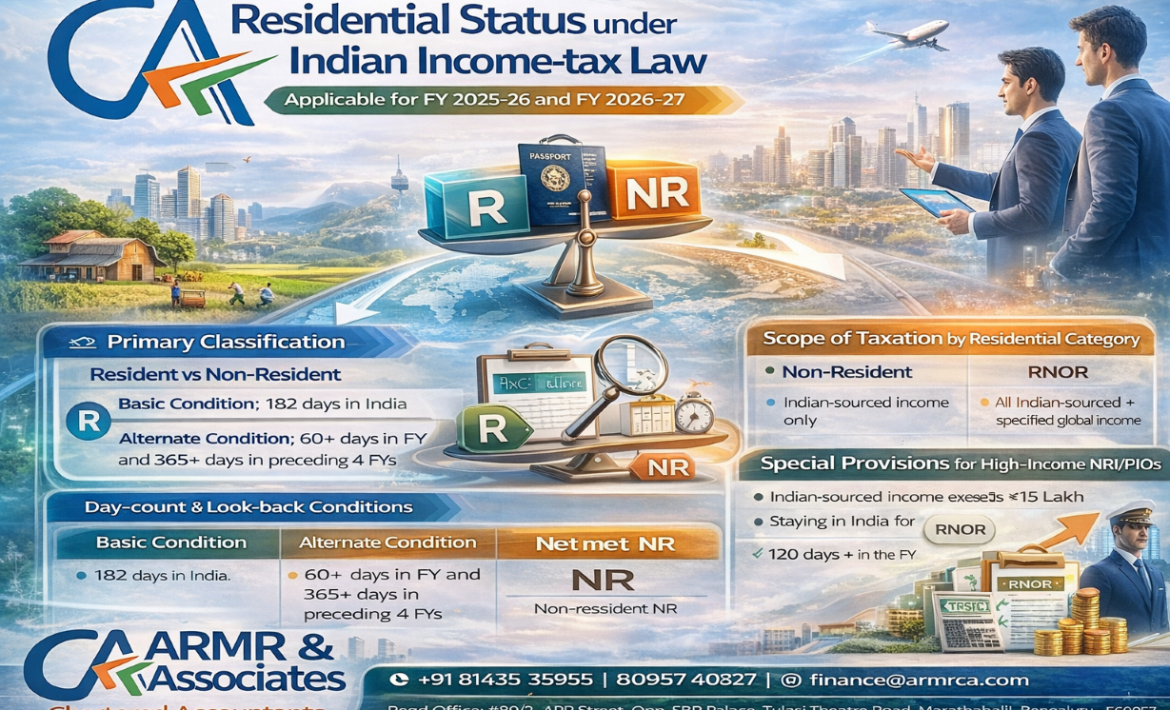

Applicable for FY 2025–26 and FY 2026–27 Residential status is determined separately for each financial…

The Ministry of Finance has notified the Income-tax Rules, 2026 in exercise of its powers…

Capital gains arise under section 45 on transfer of a “capital asset” as defined in…