Tax Deducted at Source (TDS) on cash withdrawals discourages excessive cash usage and promotes digital transactions in India. Significant changes introduced in the Income Tax Act 2025 simplify compliance by removing ITR-linked complexities, effective from FY 2026-27 (April 1, 2026).

Old Rules Under Section 194N (Pre-April 2026)

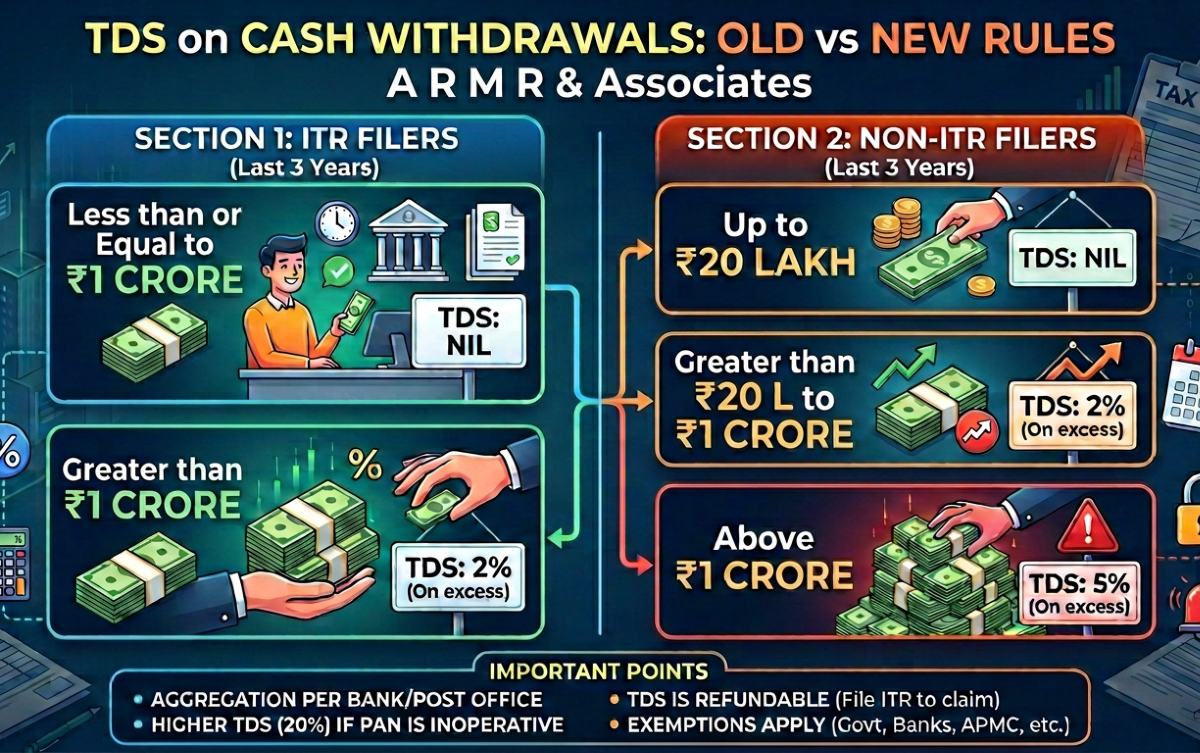

Prior to the Income Tax Act 2025, Section 194N mandated TDS by banks, co-operative banks, and post offices on aggregate cash withdrawals exceeding specified thresholds in a financial year.

Thresholds and rates depended on the withdrawer’s Income Tax Return (ITR) filing status for the three preceding assessment years:

| Cash Withdrawal Amount | TDS Rate (ITR Filed for Any of 3 Prior AYs) | TDS Rate (No ITR Filed for All 3 Prior AYs) |

|---|---|---|

| Up to ₹1 Crore | Nil | Up to ₹20 Lakh: Nil; ₹20 Lakh to ₹1 Crore: 2% |

| Above ₹1 Crore | 2% on excess | 5% on excess |

This structure penalized non-filers with a lower ₹20 lakh threshold and higher 5% rate beyond ₹1 crore, aiming to enforce tax compliance.

New Rules Under Section 393(3) (From April 2026)

The Income Tax Act 2025, via Section 393(3), retains core TDS on cash withdrawals but eliminates ITR verification burdens for payers.

Now, TDS applies uniformly at 2% on amounts exceeding ₹1 crore in aggregate cash withdrawals per financial year, regardless of filing status.

| Cash Withdrawal Amount | TDS Rate |

|---|---|

| Up to ₹1 Crore | Nil |

| Above ₹1 Crore | 2% on excess |

The removal of the ₹20 lakh slab and 5% rate addresses practical challenges for banks in checking ITR status, streamlining operations.

Key Differences: Old vs New Rules

The transition simplifies TDS application while maintaining the ₹1 crore threshold for standard cases.

- ITR Dependency: Old rules tied lower thresholds/higher rates to non-filers; new rules apply uniform 2% beyond ₹1 crore.

- Thresholds: No more ₹20 lakh slab; solely ₹1 crore for all.

- Rates: Caps at 2%; no 5% escalation.

- Payer Burden: Banks no longer verify ITRs, reducing errors.

These changes, effective FY 2026-27, align with Budget 2025 rationalization.

Who Deducts TDS and Applicability

Banks (public/private), co-operative banks, and post offices deduct TDS at withdrawal time on aggregate sums across accounts per payer.

Applies to individuals, HUFs, firms, companies; includes savings/current accounts and ATMs. Exemptions cover government, banks on own account, and notified entities.

Compliance Tips for Taxpayers

File ITRs timely to claim TDS credit in your return, as it’s refundable if excess. Opt for digital payments to avoid TDS; track annual withdrawals per institution (not PAN-wide).

Lower deduction certificates (Form 13) now apply broadly under Section 395. Businesses should maintain records for audits.

Impact on Businesses and Individuals

Simplified rules ease cash management for compliant taxpayers but retain deterrence against high cash reliance. Small businesses benefit from no ITR checks, though large withdrawals still attract 2% TDS.

This shift supports India’s digital economy push post-demonetization.