TDS under GST: Meaning and Objective

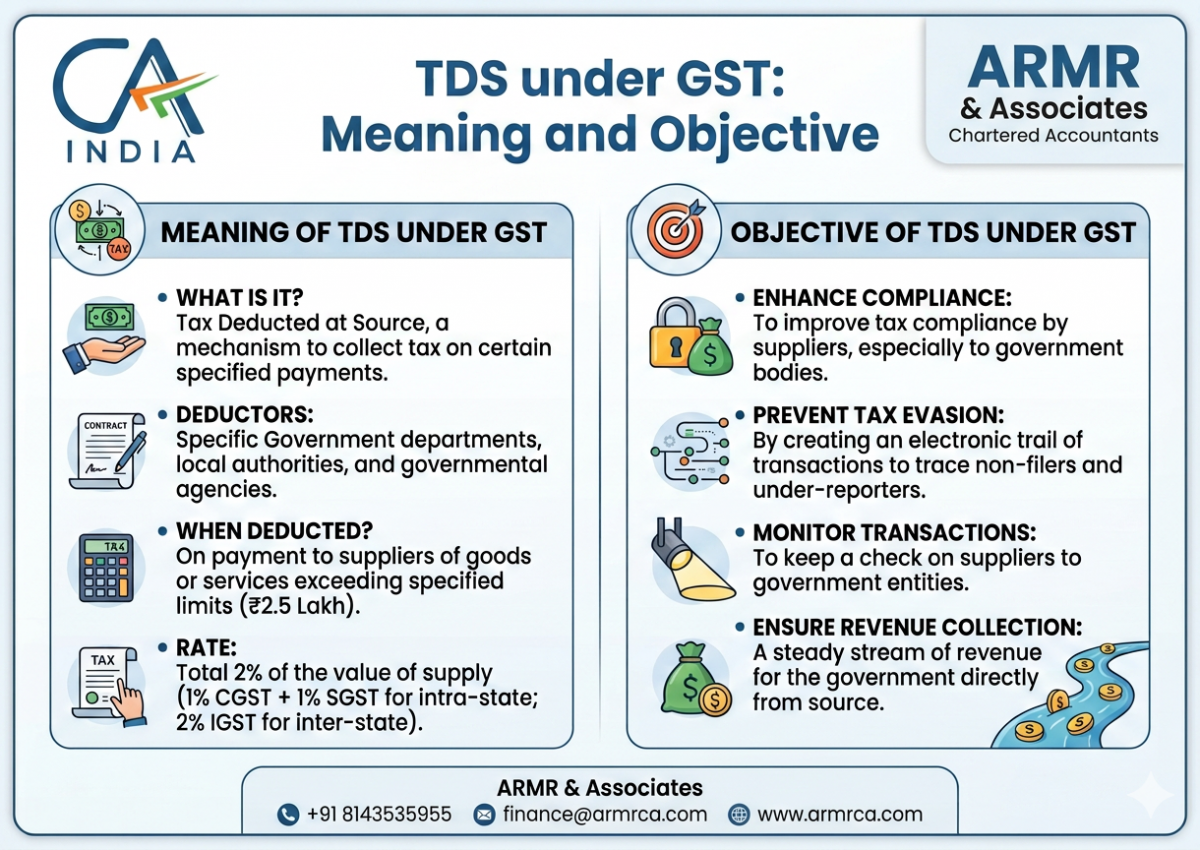

Tax Deducted at Source (TDS) under GST is a mechanism through which the government collects tax at the point of payment for specified supplies of goods or services. It helps to track transactions, ensure better tax compliance, and secure timely collection of revenue from notified recipients.

Who is liable to deduct TDS under GST? (Section 51)

As per section 51 of the CGST Act, the following persons are required to deduct TDS on notified supplies:

- Department or establishment of the Central Government or State Government.

- Local Authorities.

- Governmental agencies.

- Any other category of persons as may be notified by the Government on the recommendation of the GST Council.

Vide Notification No. 50/2018 – Central Tax dated 13 September 2018, the following additional entities were notified as TDS deductors with effect from 1 October 2018:

- Any authority, board or body set up by an Act of Parliament or State Legislature, or established by any Government, with at least 51% participation by way of equity or control.

- Societies established by the Central Government, State Government or local authority under the Societies Registration Act, 1860.

- Public Sector Undertakings (PSUs).

For such persons, obtaining separate GST registration as a tax deductor is mandatory; the usual threshold limit does not apply.

When does TDS under GST apply?

TDS under GST applies when a notified recipient (deductor) makes payment to a supplier of taxable goods or services under a contract where the taxable value exceeds ₹2.50 lakh.

Key conditions for applicability:

- The aggregate value of taxable supply under a single contract must exceed ₹2.50 lakh.

- The value for this limit is computed on the taxable value only, excluding CGST, SGST, IGST, UTGST and Cess.

If a contract involves both taxable and exempt supplies, TDS is applicable only when the taxable portion of the contract exceeds ₹2.50 lakh.

In simple terms, once the taxable value under a single contract crosses ₹2.50 lakh, the notified recipient is required to deduct TDS from payments made to the supplier, but only on the taxable component and not on GST itself.

Situations where TDS under GST is not required

TDS under GST is not to be deducted in the following situations:

Where the total taxable value of supply under a single contract is less than or equal to ₹2.50 lakh.

Where the contract value exceeds ₹2.50 lakh but the taxable portion within that contract is less than or equal to ₹2.50 lakh (for example, high exempt value with low taxable value).

Where the supply is wholly exempt, nil-rated, or not liable to GST.

Where the location of the supplier and the place of supply are in one State/UT, but the location of the recipient (deductor) is in another State/UT; in such cases, TDS is not to be deducted as credit would not be available.

Where the transaction is covered under Schedule III of the CGST Act (neither supply of goods nor services), such as services by an employee to employer, etc.

Where tax is payable by the recipient under reverse charge mechanism (RCM); here the entire tax is paid by the recipient and there is no TDS.

These carve-outs ensure that TDS operates only in specific, trackable B2G/PSU-type transactions and not across all supplies.

Rate of TDS under GST

TDS under GST is deducted at the rate of 2% on the taxable value of supplies.

For intra‑State supplies, TDS is deducted at 1% CGST + 1% SGST/UTGST.

For inter‑State supplies, TDS is deducted at 2% IGST.

The rate is applied on the taxable value (before GST), as reflected in the tax invoice.

Time and mode of depositing TDS

The amount of TDS deducted must be deposited with the government within 10 days from the end of the month in which deduction is made.

Payment is made through the electronic cash ledger of the deductor on the GST portal, using the relevant challan.

Failure to deposit TDS within the stipulated time attracts interest at the applicable rate under GST law on the delayed amount.

TDS Certificate – Form GSTR‑7A

Every deductor who deducts TDS under GST must issue a TDS certificate in Form GSTR‑7A to the supplier (deductee).

Key points:

GSTR‑7A is a system‑generated certificate based on details furnished in GSTR‑7 by the deductor and accepted by the deductee.

The certificate must be made available within 5 days of depositing TDS to the government.

If the deductor fails to issue the certificate within 5 days, a late fee of ₹100 per day per Act (₹100 CGST + ₹100 SGST) may be levied, subject to a maximum of ₹5,000 under each Act.

Once generated, the TDS so deposited is credited to the electronic cash ledger of the deductee, which can then be used to discharge tax or other dues.

TDS Return – Form GSTR‑7

Every registered TDS deductor is required to file a monthly return in Form GSTR‑7.

Due date: 10th of the month following the month in which TDS was deducted.

The return contains invoice‑wise details of suppliers, GSTIN, contract value, taxable value, and tax deducted.

In case the supplier is unregistered, the name of the supplier is reported in place of GSTIN in GSTR‑7.

Once GSTR‑7 is correctly filed and accepted, the corresponding TDS credit gets auto‑populated in the electronic cash ledger of the supplier.

Late filing of GSTR‑7 can attract late fees and interest as per GST provisions.