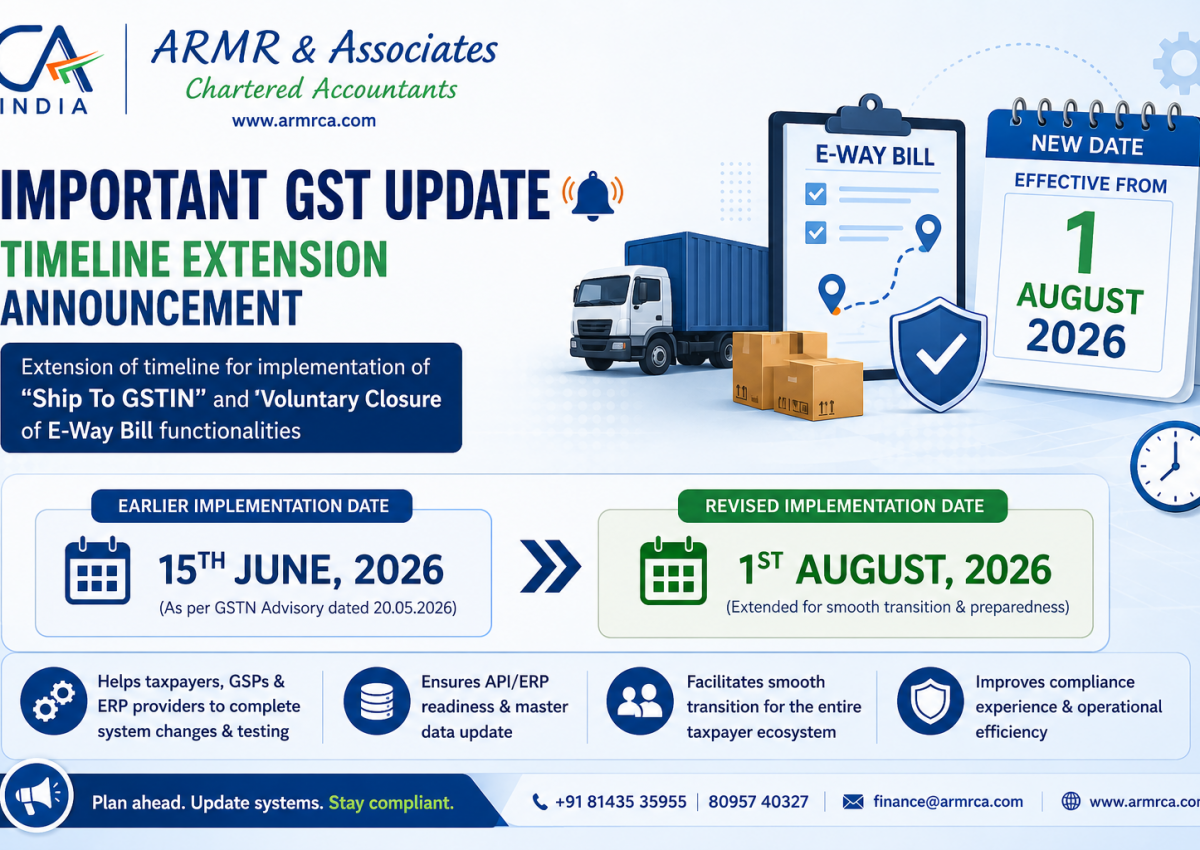

The GSTN has extended the implementation timeline for two important E-Way Bill changes that were originally scheduled to come into effect from 15th June 2026. As per the latest advisory dated 9th June 2026, the revised implementation date for both functionalities is now 1st August 2026.

This extension gives taxpayers, transporters, ERP providers, GSPs and compliance teams additional time to update their systems, test workflows and complete operational readiness. Businesses should use this extended window wisely, because the changes are compliance-sensitive and will affect daily dispatch and billing processes.

What has GSTN announced?

GSTN has postponed the implementation of the following two functionalities in the E-Way Bill system:

- Mandatory capture of “Ship To GSTIN” in Bill-To / Ship-To transactions.

- Voluntary closure of E-Way Bill functionality.

These changes were earlier proposed to be implemented from 15th June 2026, but based on representations received from trade and industry, the date has now been extended to 1st August 2026.

Why was the implementation postponed?

According to the advisory, various stakeholders sought additional time due to the practical challenges involved in implementing these changes. The key concerns included:

- System-level changes in accounting, billing and ERP software.

- Time required for testing by API users and ERP providers.

- Need for updating customer and transaction master data.

- Overall operational readiness across the taxpayer ecosystem.

Recognising these concerns, GSTN has granted more time to facilitate a smoother transition and avoid disruption in business operations.

What does mandatory “Ship To GSTIN” mean?

In many transactions, especially in business supply chains, the invoice may be raised to one party while the goods are delivered to another location or GSTIN. These are commonly referred to as Bill-To / Ship-To transactions.

Under the upcoming change, the E-Way Bill system will require mandatory capture of the “Ship To GSTIN” in such cases. This means businesses will have to ensure that:

- Their customer master properly records both Bill-To and Ship-To details.

- ERP or billing software is capable of capturing the correct Ship-To GSTIN.

- Teams involved in invoicing and dispatch understand when and how to enter this information correctly.

This requirement is intended to improve tracking of actual movement of goods and reduce data mismatches in GST compliance systems.

What is voluntary closure of E-Way Bill?

The second functionality relates to voluntary closure of E-Way Bills. This means taxpayers may be given the option to mark an E-Way Bill as closed once the underlying transaction or movement is completed.

This can help in:

- Better tracking of completed consignments.

- Reducing confusion over old or inactive E-Way Bills.

- Maintaining cleaner records for reconciliation and internal control.

- Improving visibility in logistics and compliance monitoring.

For businesses handling large dispatch volumes, this feature can become an important operational control tool.

Revised effective date

Both the above functionalities will now be implemented from:

1st August 2026

instead of the earlier proposed date of:

15th June 2026

Therefore, taxpayers now have additional time to complete the required changes before the revised implementation date.

What should taxpayers do now?

Businesses should not treat this extension as a reason to postpone action. Instead, they should use this time for structured preparation. The following steps are advisable:

1. Review customer and consignee master data

Check whether customer records properly contain:

- Bill-To GSTIN

- Ship-To GSTIN

- Delivery address

- State and place of supply details

Any mismatch or incomplete data may lead to errors once the functionality becomes mandatory.

2. Coordinate with ERP / software vendors

Businesses using ERP systems, billing software, or API-based E-Way Bill solutions should immediately speak to their software provider and confirm:

- Whether the Ship-To GSTIN field has been enabled

- Whether Bill-To / Ship-To logic has been updated

- Whether voluntary closure functionality will be supported

- Whether testing can be completed before 1st August 2026

3. Conduct internal testing

Before the effective date, businesses should run sample transactions to ensure that:

- E-Way Bills generate correctly for Bill-To / Ship-To cases

- GSTIN mapping is accurate

- Internal teams know the revised workflow

- Any validation errors are identified in advance

4. Train dispatch, billing and accounts teams

Practical implementation will depend heavily on the teams actually generating invoices and E-Way Bills. Businesses should therefore give clear internal instructions to:

- Billing staff

- Logistics teams

- Dispatch coordinators

- Accounts and compliance personnel

A simple internal SOP can help avoid last-minute confusion.

5. Plan process for voluntary closure

Where relevant, businesses should decide:

- Who will close the E-Way Bill

- At what stage closure should happen

- What supporting records will be kept

- How closure will be tracked internally

This is especially important for businesses with large volume dispatches or decentralised dispatch teams.

Why this update is important

Although this is only an extension of timeline, the advisory is significant because it confirms that GSTN is moving ahead with these functionalities. Once implemented, they may directly affect:

- Accuracy of E-Way Bill generation

- Dispatch workflow

- ERP integration

- GST data matching and reconciliation

- Internal controls over goods movement

Businesses that do not prepare in advance may face avoidable operational issues and compliance errors.

Final note

The extension from 15th June 2026 to 1st August 2026 provides a useful opportunity for businesses to strengthen their systems and processes. Taxpayers, transporters, ERP providers and GST consultants should use this period to complete master updates, system changes, testing and user training.

Timely preparation will help ensure a smooth rollout and reduce the risk of disruption once the revised implementation date becomes effective.