1. Introduction

Indexation has historically been one of the most powerful tax‑saving tools for long‑term investors in India. By adjusting the purchase cost of an asset for inflation, indexation significantly reduces taxable capital gains.

However, with the new capital gains tax regime introduced through the Finance Act 2024, the availability of indexation has undergone major changes. For AY 2026‑27, indexation benefits have been removed for most asset classes, except for a limited grandfathering window for certain real estate assets.

This article explains the impact of these changes and how taxpayers should plan their investments and asset disposals.

2. What Is Indexation?

Indexation adjusts the cost of an asset using the Cost Inflation Index (CII) notified annually by the CBDT.

The formula is:

Indexed Cost of Acquisition = Cost of Acquisition × (CII of year of sale ÷ CII of year of purchase)

This increases the cost base and reduces taxable long‑term capital gains (LTCG).

3. Capital Gains Tax Rules Applicable for AY 2026‑27

A. Equity Shares & Equity Mutual Funds

- LTCG tax rate: 12.5%

- Exemption: ₹1.25 lakh per year

- Indexation: Not allowed

B. Debt Mutual Funds, Gold Funds, Bonds

- Units acquired on or after 1 April 2023

- Taxation: At slab rate, irrespective of holding period

- Indexation: Not allowed

C. Gold, Silver, and Other Assets

- LTCG tax rate: 12.5%

- Indexation: Not allowed

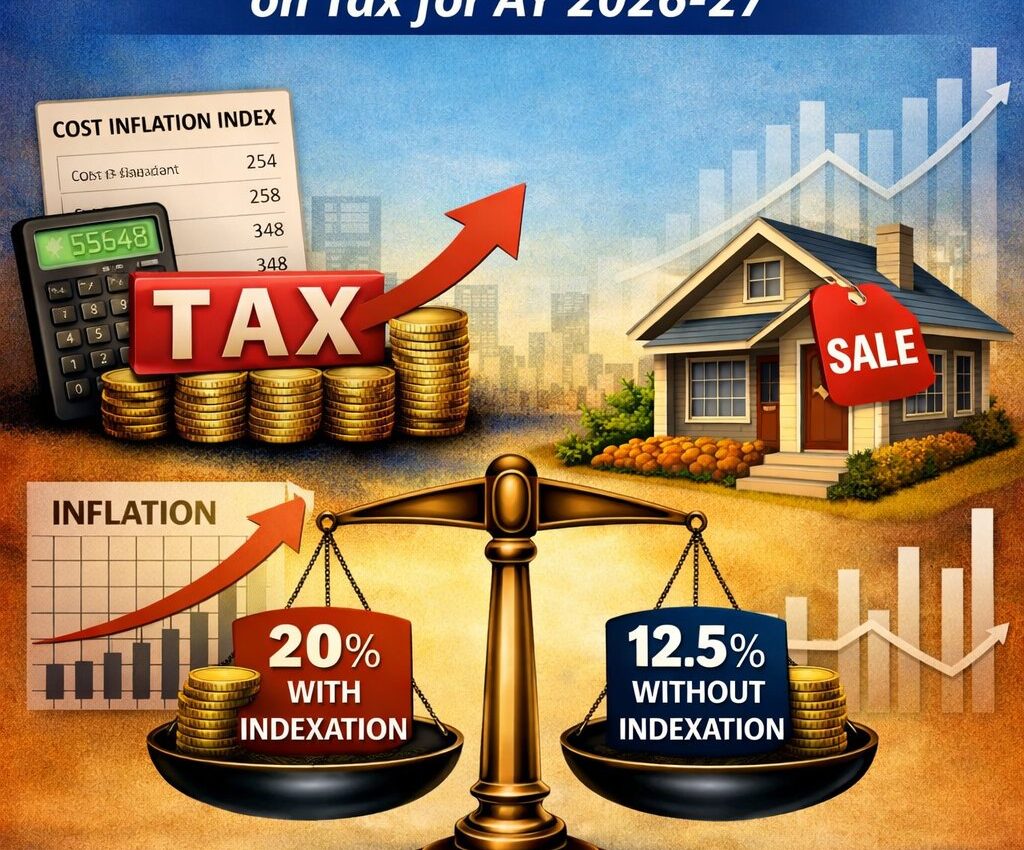

D. Real Estate (Land & Building)

This is the only category where indexation may still apply.

| Purchase Date | Tax Rate Options | Indexation |

| On or before 22 July 2024 | 12.5% (no indexation) OR 20% (with indexation) | Allowed |

| On or after 23 July 2024 | 12.5% flat | Not allowed |

This one‑time grandfathering is the only remaining indexation benefit for AY 2026‑27.

4. Why the Removal of Indexation Matters

1. Higher Tax Outgo

Earlier, many assets enjoyed 20% tax with indexation, significantly reducing tax liability.

Now, most assets are taxed without indexation, increasing taxable gains.

2. Reduced Attractiveness of Debt Mutual Funds

Debt MFs now face slab‑rate taxation, making them less tax‑efficient compared to:

- PPF

- Sovereign Gold Bonds

- Tax‑free bonds

3. Real Estate Requires Strategic Planning

For properties purchased before 22 July 2024, taxpayers must compute tax both ways and choose the lower option.

5. Numerical Illustration: With vs Without Indexation

Example:

Property purchased in FY 2015‑16 for ₹50,00,000

Sold in FY 2025‑26 for ₹1,50,00,000

CII (2015‑16 = 254, 2023‑24 = 348)

Option 1: 20% Tax With Indexation

Indexed Cost = 50,00,000 × (348 ÷ 254) = ₹68,50,000

Taxable LTCG = 1,50,00,000 – 68,50,000 = ₹81,50,000

Tax @ 20% = ₹16,30,000

Option 2: 12.5% Tax Without Indexation

Taxable LTCG = 1,50,00,000 – 50,00,000 = ₹1,00,00,000

Tax @ 12.5% = ₹12,50,000

Conclusion:

The taxpayer should choose 12.5% without indexation, as it results in lower tax.

6. Asset‑Wise Impact Summary (AY 2026‑27)

| Asset Class | Tax Rate | Indexation |

| Equity | 12.5% | No |

| Equity MFs | 12.5% | No |

| Debt MFs | Slab rate | No |

| Gold/Silver | 12.5% | No |

| Real Estate (pre‑22 July 2024 purchase) | 12.5% or 20% | Yes (optional) |

| Real Estate (post‑23 July 2024 purchase) | 12.5% | No |

7. Tax Planning Tips for AY 2026‑27

A. For Real Estate Owners

- Compute tax under both options if eligible for indexation.

- Use exemptions under Sections 54, 54F, 54EC to reduce tax.

B. For Debt MF Investors

- Consider shifting to more tax‑efficient instruments.

- Time redemptions in years with lower income.

C. For Equity Investors

- Book LTCG up to ₹1.25 lakh annually to maximize exemption.

8. Conclusion For AY 2026‑27, indexation benefits have been largely phased out, except for a limited window for older real estate assets. This marks a major shift in India’s capital gains taxation framework. Investors must now evaluate tax implications more carefully, especially when selling property or restructuring debt‑based investments