Objective

This guide is designed to be the most comprehensive resource on GST appeals in India, covering the complete litigation lifecycle—from the receipt of a GST notice to the final appeal before the Supreme Court. It is intended for taxpayers, Chartered Accountants, tax practitioners, advocates, CFOs, finance teams, and business owners.

What Makes This Guide Different?

✔ Every important GST notice

✔ Every stage of litigation

✔ Applicable legal provisions

✔ Time limits

✔ Reply strategy

✔ Hearing process

✔ Appeal drafting

✔ Mandatory pre-deposit

✔ Recovery proceedings

✔ Tribunal appeals

✔ High Court remedies

✔ Supreme Court appeals

✔ Practical checklists

✔ Judicial precedents

✔ Frequently asked questions

Proposed Structure

PART 1 – Understanding GST Litigation

Chapter 1 – Introduction

Chapter 2 – Why GST Notices are Issued

Chapter 3 – Types of GST Proceedings

Chapter 4 – Litigation Flow Chart

Chapter 5 – Authorities under GST

Chapter 6 – Important Definitions

PART 2 – Every GST Notice Explained

Create separate chapters for:

Registration Notices

- REG-03

- REG-17

- REG-23

- REG-27

- REG-31

For each notice explain:

• Legal Provision

• Purpose

• When issued

• Reply Time

• Documents Required

• Practical Example

• Consequences of Non-response

• Next Course of Action

Assessment Notices

Cover the ASMT series comprehensively.

Explain:

Self-assessment

Provisional assessment

Scrutiny assessment

Best judgment assessment

Summary assessment

Demand Notices

Cover every DRC Form.

Include:

DRC-01

DRC-01A

DRC-03

DRC-06

DRC-07

DRC-13

DRC-16

DRC-22

etc.

Audit Proceedings

Explain:

Department Audit

Special Audit

Taxpayer Rights

Reply Process

Appeal Options

Search & Seizure Proceedings

Inspection

Search

Seizure

Detention

Confiscation

MOV Forms

Appeal Process

Refund Proceedings

Refund Rejection

Export Refund

Inverted Duty Refund

Appeal Procedure

PART 3 – Reply to GST Notices

How to analyse notice

Preparing documentary evidence

Legal research

Drafting reply

Uploading reply

Attending personal hearing

Additional submissions

Natural justice

PART 4 – Understanding GST Orders

Assessment Order

Demand Order

Penalty Order

Cancellation Order

Refund Order

Detention Order

Confiscation Order

Explain:

Legal effect

Recovery implications

Appealability

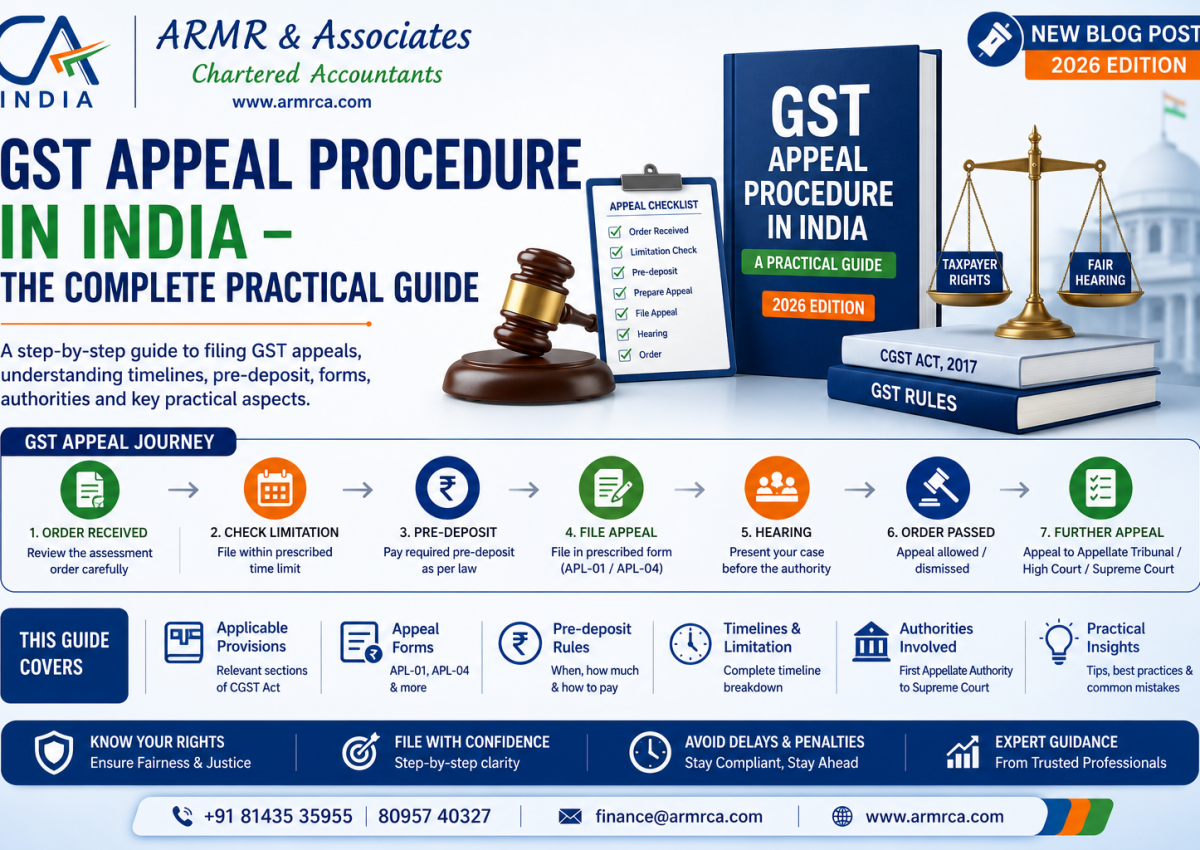

PART 5 – First Appeal (Section 107)

Who can file

Who cannot file

Orders appealable

Orders not appealable

Time limit

Delay condonation

Mandatory pre-deposit

Documents required

Drafting statement of facts

Grounds of appeal

Additional evidence

Personal hearing

Order of Appellate Authority

PART 6 – Mandatory Pre-deposit

Explain with illustrations.

Example 1

Tax demanded ₹20 Lakhs

Admitted ₹5 Lakhs

Disputed ₹15 Lakhs

Calculate mandatory payment.

Example 2

Penalty-only demand

Example 3

Interest dispute

Example 4

Mixed demand

Include:

Common mistakes

Frequently misunderstood provisions

Refund of pre-deposit

PART 7 – Recovery Proceedings

When recovery starts

Whether recovery is stayed

Bank attachment

Property attachment

Adjustment against refunds

Auction

How to obtain relief

PART 8 – Appeal Before GST Appellate Tribunal

Jurisdiction

Benches

Procedure

Additional pre-deposit

Hearing

Orders

Rectification

Restoration

PART 9 – Appeal Before High Court

Substantial question of law

Maintainability

Limitation

Writ jurisdiction

Interim relief

Stay petitions

PART 10 – Appeal Before Supreme Court

Appealable matters

Special Leave Petition

Important principles

PART 11 – Special Categories of Appeals

Cancellation of GST Registration

Input Tax Credit denial

Fake Invoice matters

Refund rejection

Detention of goods

Confiscation

E-way Bill penalty

RCM disputes

Classification disputes

Valuation disputes

Export disputes

PART 12 – Drafting Appeals

Model:

Statement of Facts

Grounds

Prayer

Additional Grounds

Compilation Index

Paper Book

Written Arguments

PART 13 – Important Judicial Decisions

Arrange judgments topic-wise.

Natural Justice

Limitation

Pre-deposit

Input Tax Credit

Penalty

Registration

Recovery

Refund

Detention

Each case should include:

Facts

Issue

Decision

Practical takeaway

PART 14 – Ready Reckoner Tables

Create quick-reference tables for:

Notice-wise Reply Period

Appeal Time Limits

Delay Condonation

Forms

Authorities

Pre-deposit

Recovery

Next Remedy

Applicable Sections

PART 15 – Practical Flowcharts

Flowchart 1

Notice → Reply → Hearing → Order

↓

Appeal

↓

Tribunal

↓

High Court

↓

Supreme Court

Flowchart 2

Demand Order

↓

Should You Pay?

↓

Should You Appeal?

↓

Pre-deposit

↓

Stay

↓

Recovery

Flowchart 3

Cancellation of Registration

↓

Reply

↓

Order

↓

Revocation

↓

Appeal

PART 16 – Practical Checklists

Checklist before replying

Checklist before hearing

Checklist before appeal

Checklist before Tribunal

Checklist before High Court

PART 17 – Frequently Asked Questions

Prepare approximately 75–100 practical questions based on real client situations.

Examples include:

Can I file an appeal after the limitation period?

Can I appeal without paying the pre-deposit?

Can I challenge only the penalty?

Can I submit additional evidence?

Can multiple orders be challenged in one appeal?

What happens if my appeal is dismissed for default?

Can recovery continue after filing an appeal?

PART 18 – Conclusion

The GST appeal mechanism is a structured legal remedy that enables taxpayers to challenge incorrect assessments, penalties, registration cancellations, refund rejections, and other adverse orders. Success depends on timely action, a well-prepared factual record, compliance with statutory timelines and pre-deposit requirements, and persuasive legal submissions. Businesses should respond proactively to notices and seek professional advice at the earliest stage to minimise litigation risk and improve the likelihood of a favourable outcome.